Celebrating 25 Incredible Years of Westchester Mortgage. Thank You!

October marks a special occasion for me: the 25th anniversary of the founding of my company, Westchester Mortgage!

Looking Back

A quarter-century in business is a major milestone. As I reflect on the years past, I’m filled with gratitude for all the clients I’ve had the honor of helping finance their biggest asset. My work has always been about guiding you through one of the most significant financial decisions of your life.

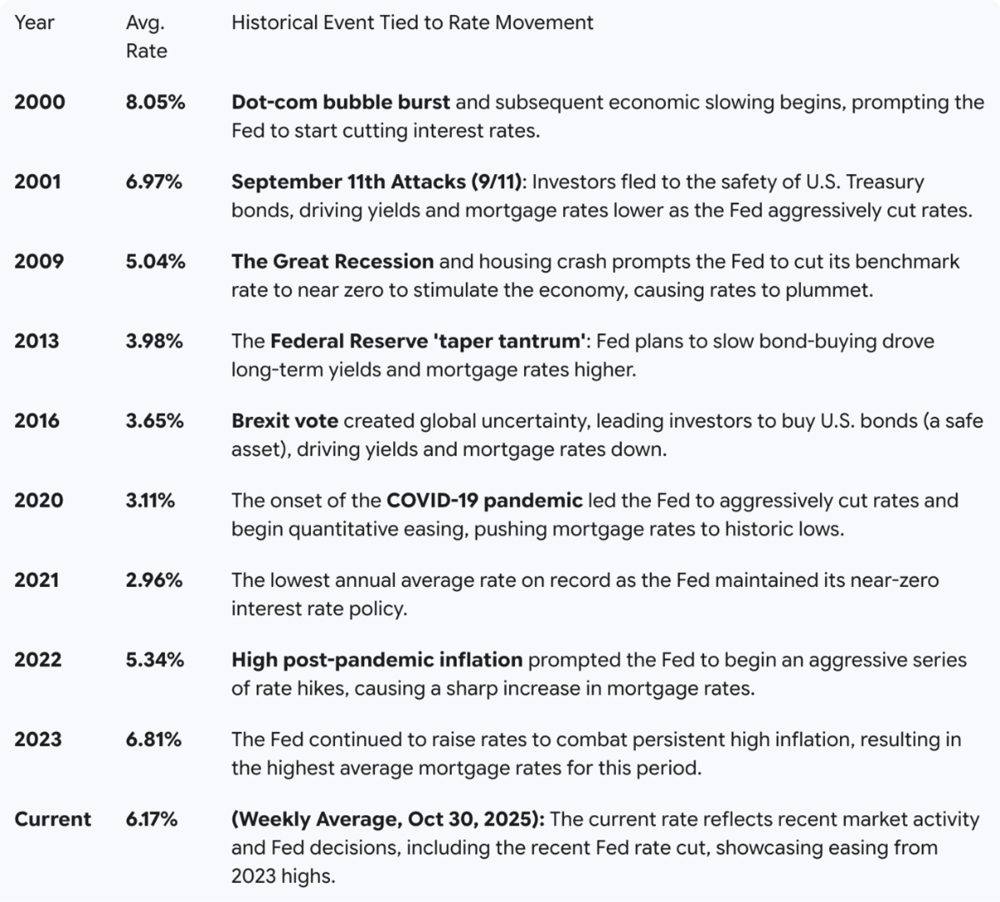

The one constant has been the fluctuating 30-year fixed mortgage rate. From the aftermath of 9/11 to the Great Recession. From historic lows during the pandemic to the recent battle against inflation. Virtually every major economic and world event has had a direct impact on your borrowing costs and purchasing power.

I thought it might be interesting to look back at mortgage rates since 2000, tying these changes to the historical events that drove them.

How many of these events do you remember?

Looking Ahead

As the table above shows, mortgage rates are not static; they are a direct reflection of the global and domestic environment. Over the last 25 years, I’ve personally helped clients through times that were a little scary. But the most important lesson I’ve learned is that even the most frightening global events are often followed by periods of economic change and new opportunity.

The fact that the current rate has eased to 6.17% shows that the market is always moving and new windows of opportunity are always opening. This recent drop, supported by the Federal Reserve’s decision to cut interest rates in late October, is a significant shift from the 2023 average of 6.81%. This shows that positive changes are happening right now.

While we can’t predict the future, we know that these changes are part of the natural cycle of the market. Rather than fearing uncertainty, let’s approach it with the confidence that comes from experience and preparation.

My promise to you, as my valued customer, is that I will continue to be here, just as I have for 25 years, to provide the focused, expert guidance you need to navigate whatever the next chapter of the housing market brings. We’ll ride the cycles together.

If you’re planning to start your homebuying journey now or into early 2026, please reach out. I’ll help you get prepped and positioned so you can move quickly and confidently to find your dream home.

Home Improver: Leave the Leaves for a Better Lawn with Mulch Mowing

Here’s a tip: Skip the back-breaking raking and the endless yard waste bags. Your leaves are a free, natural fertilizer and a secret weapon for a healthier lawn. By chopping your fallen leaves into dime-sized pieces right on the grass using your lawnmower, you are practicing what’s known as mulch mowing.

As these tiny pieces settle into the turf, they decompose over the winter, returning valuable nutrients like nitrogen and phosphorus back to your soil. This simple practice helps improve soil structure, suppresses early spring weeds like dandelions, and significantly reduces the amount of expensive fertilizer you will need next spring.

As these tiny pieces settle into the turf, they decompose over the winter, returning valuable nutrients like nitrogen and phosphorus back to your soil. This simple practice helps improve soil structure, suppresses early spring weeds like dandelions, and significantly reduces the amount of expensive fertilizer you will need next spring.

Beyond the benefits to your lawn, mulch-mowing is the responsible choice for the planet. When leaves are raked, bagged, and sent to a landfill, they take up unnecessary space and decompose without oxygen, which releases methane (a potent greenhouse gas) that contributes to climate change.

By using your mower to return the leaves to the soil, you avoid contributing to landfill waste, save money on bags and disposal fees, and provide a vital habitat for those beneficial insects and microorganisms that keep your yard healthy.

Important: Be sure you can still see at least half of the grass through the shredded layer of leaves (see image above) to prevent smothering the turf.

Let’s stay ahead of this. Here’s your checklist:

Let’s stay ahead of this. Here’s your checklist: Did you know your ceiling fans can help lower heating costs? Most people think of ceiling fans as a summertime necessity, but they can actually help you stay warmer in the cooler months, too. The secret is in the small switch on the motor housing that changes the blade direction.

Did you know your ceiling fans can help lower heating costs? Most people think of ceiling fans as a summertime necessity, but they can actually help you stay warmer in the cooler months, too. The secret is in the small switch on the motor housing that changes the blade direction.

Many homeowners set up their policy at closing and never revisit it. The problem? A lot can change in just a few years. The cost to rebuild your home may have gone up. You might have made improvements like finishing a basement, updating a kitchen or adding solar panels. Or maybe you’ve acquired higher-value personal items like jewelry, artwork or electronics. If your policy hasn’t been updated to reflect these changes, you could be underinsured. That could lead to financial stress in the aftermath of unfortunate events.

Many homeowners set up their policy at closing and never revisit it. The problem? A lot can change in just a few years. The cost to rebuild your home may have gone up. You might have made improvements like finishing a basement, updating a kitchen or adding solar panels. Or maybe you’ve acquired higher-value personal items like jewelry, artwork or electronics. If your policy hasn’t been updated to reflect these changes, you could be underinsured. That could lead to financial stress in the aftermath of unfortunate events. Once the danger of frost has passed, usually after Mother’s Day, you can transplant your tomatoes outdoors. Choose a spot with full sun and well-drained soil, and don’t forget to

Once the danger of frost has passed, usually after Mother’s Day, you can transplant your tomatoes outdoors. Choose a spot with full sun and well-drained soil, and don’t forget to  Reduce Humidity: Silverfish love moisture, so use a dehumidifier in damp areas like basements, bathrooms, and laundry rooms. Fix any leaky pipes or faucets to cut off their water supply.

Reduce Humidity: Silverfish love moisture, so use a dehumidifier in damp areas like basements, bathrooms, and laundry rooms. Fix any leaky pipes or faucets to cut off their water supply. Deodorize and Freshen Spaces: Sprinkle baking soda in your fridge, trash cans, or shoes to neutralize odors. Its odor-absorbing power works wonders in keeping spaces smelling fresh without artificial scents.

Deodorize and Freshen Spaces: Sprinkle baking soda in your fridge, trash cans, or shoes to neutralize odors. Its odor-absorbing power works wonders in keeping spaces smelling fresh without artificial scents. Weather Stripping: Apply adhesive weather-stripping tape around door and window frames. This simple solution seals gaps and stops drafts, making your home more energy-efficient.

Weather Stripping: Apply adhesive weather-stripping tape around door and window frames. This simple solution seals gaps and stops drafts, making your home more energy-efficient. Switch to Orange Light Bulbs

Switch to Orange Light Bulbs