The Ripple Effect: Why Mortgage Rates Defy the Headlines

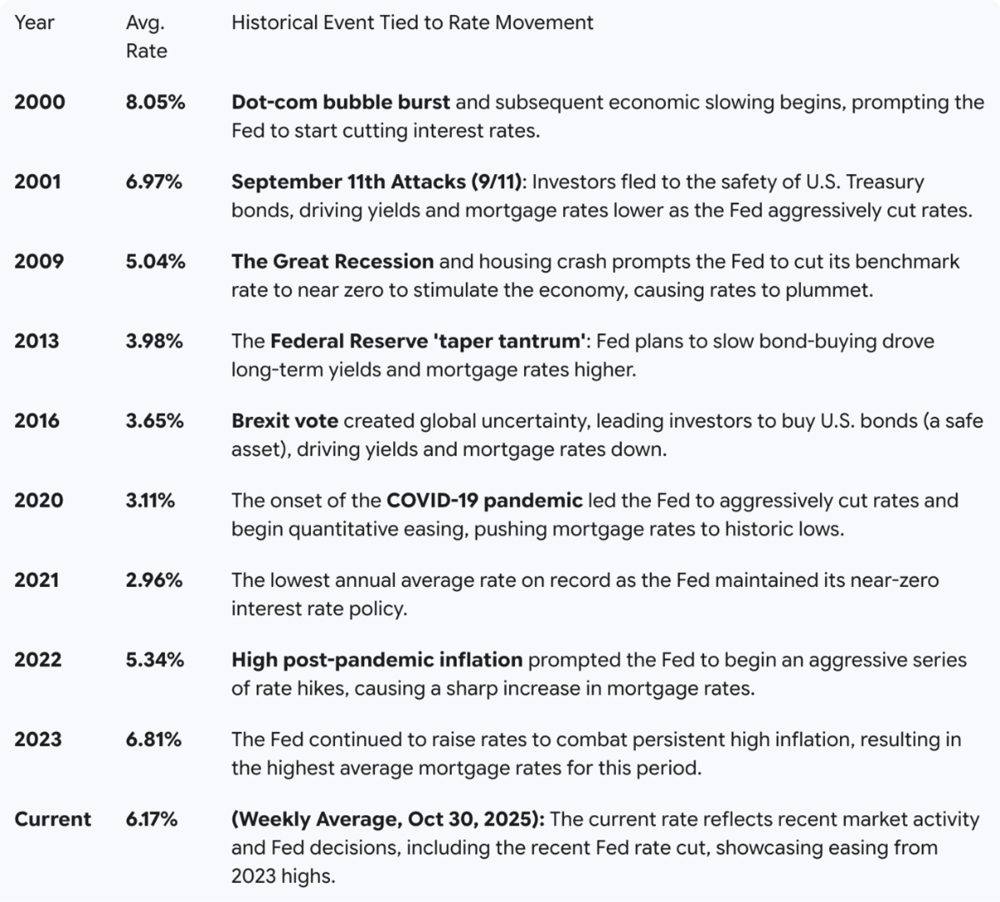

At the start of 2025, many economic experts and major news outlets shared a similar forecast: Mortgage rates would steadily decline throughout the year. If you follow the housing market, you likely saw those headlines and were filled with hope. Realtor.com and Fannie Mae initially predicted that the 30-year fixed rate would average near 6.3% and perhaps even touch the high 5% range by year-end. However, as we look at the current landscape, it is clear that those predictions did not materialize as expected.

Understanding the Global Connection

Understanding why rates stayed higher requires looking at the world economy. Financial markets thrive on stability, and the past year has been defined by the opposite. Significant global events create a ripple effect that starts with general economic volatility. This uncertainty quickly moves into the bond market, which is the primary driver of mortgage interest rates.

When global tension or economic shifts occur, investors often move their money into safer assets like 10-year Treasury bonds. This shift in demand changes the yield on those bonds, and mortgage rates typically follow that trajectory. Because of unpredictable events early in the year, including shifting trade policies and persistent inflation data, the stability required for a rate drop never quite took hold. Instead, the market reacted to each new headline with caution.

Why Local Markets React to Global News

This chain reaction is why your local housing market often feels the impact of events happening thousands of miles away. Lenders must account for this risk when they set their pricing for the day. While a headline might promise a drop based on one economic report, a single global event can negate that progress in a matter of hours.

Instead of waiting for a perfect rate that may be delayed by further global shifts, many homeowners are focusing on what they can control. Assessing your personal financial goals and the equity in your home remains the most reliable way to make a move. Markets will always experience periods of volatility, but your long-term housing needs are often more important than timing a short-term dip in the bond market.

Breaking Down the Headlines

To help understand the gap between the news and reality, it helps to look at the lag time in the industry. Headlines often report on what the Federal Reserve might do in the future. Mortgage rates, however, react to what the market is doing right now.

In early 2025, while headlines predicted “potential relief,” the bond market was already bracing for volatility. This explains why you might hear good news on your favorite news channel while the actual rates at the closing table remain steady or even tick upward.

If you’re planning to start your homebuying journey in 2026, please reach out. I’ll help you get prepped and positioned so you can move quickly and confidently to find your dream home.

Home Improver: Inspect Your Home After a Snowy, Wet Winter

With April starting next week, the forecast is already calling for some rain. This transition is especially important this year. After a winter that brought significantly more snow to Massachusetts than we have seen in recent years, the ground is already saturated. As those “April showers” begin, your basement is at a higher risk for moisture issues.

Look for Surface Indicators

Start by examining the walls and floor for efflorescence, which is a white, powdery mineral deposit left behind by evaporating water. While it may look like mold, it is actually a sign that moisture is seeping through the concrete. If you see dark spots or staining on drywall and floor joists, these are more likely to be mold or mildew.

Check the perimeter of the room for any musty odors. A damp smell often indicates that humidity levels are too high, even if you cannot see standing water. Using a hygrometer to monitor humidity is an easy way to stay informed. Maintaining a level below 50% is generally ideal for preventing growth.

Inspect Your Systems Before the Rain

If you have one, verify that your sump pump is clearing water effectively by pouring a bucket of water into the pit to trigger the float switch. This is a critical step to take before the upcoming rain arrives.

You should also look at the base of your water heater and any visible plumbing for slow drips that could contribute to local dampness.

Check the Exterior Drainage

Many basement moisture problems actually start outside the home. With the heavy snow piles finally melted, ensure your gutters are clear of any debris left behind by winter storms.

Confirm that your downspouts direct water at least five feet away from the foundation. Properly grading the soil so it slopes away from the house helps keep the basement dry by preventing spring rain from pooling against the exterior walls.

Stay safe and dry and enjoy the warming weather!

The Art of Mixing Metals

The Art of Mixing Metals Here are three simple ways strengthen your WiFi at home.

Here are three simple ways strengthen your WiFi at home.

1. Tune-Up Your Snow Blower

1. Tune-Up Your Snow Blower

As these tiny pieces settle into the turf, they decompose over the winter, returning valuable nutrients like nitrogen and phosphorus back to your soil. This simple practice helps improve soil structure, suppresses early spring weeds like dandelions, and significantly reduces the amount of expensive fertilizer you will need next spring.

As these tiny pieces settle into the turf, they decompose over the winter, returning valuable nutrients like nitrogen and phosphorus back to your soil. This simple practice helps improve soil structure, suppresses early spring weeds like dandelions, and significantly reduces the amount of expensive fertilizer you will need next spring.

Let’s stay ahead of this. Here’s your checklist:

Let’s stay ahead of this. Here’s your checklist: Did you know your ceiling fans can help lower heating costs? Most people think of ceiling fans as a summertime necessity, but they can actually help you stay warmer in the cooler months, too. The secret is in the small switch on the motor housing that changes the blade direction.

Did you know your ceiling fans can help lower heating costs? Most people think of ceiling fans as a summertime necessity, but they can actually help you stay warmer in the cooler months, too. The secret is in the small switch on the motor housing that changes the blade direction.

Did you know that

Did you know that  According to the EPA, coffee grounds contain natural compounds that are toxic to many insects, including mosquitoes. And since bugs like mosquitoes have an extremely sensitive sense of smell, they find the aroma of burning coffee grounds especially unpleasant, unlike the rest of us.

According to the EPA, coffee grounds contain natural compounds that are toxic to many insects, including mosquitoes. And since bugs like mosquitoes have an extremely sensitive sense of smell, they find the aroma of burning coffee grounds especially unpleasant, unlike the rest of us.